F Reorganizations Can Benefit Buyers and Sellers in Business Acquisitions

Certain corporate characteristics of a target company may be undesirable to potential buyers preventing them from acquiring the company. For example, the target company may be an S corporation, and the potential buyer would not qualify to be a shareholder of an S corporation under Internal Revenue Service (IRS) rules. Alternatively, the buyer may want the target company to be incorporated in a different state, such as Delaware, due to that state’s well-developed corporate law and chancery court system. In such situations and others, the seller can remove these obstacles prior to a sale by performing an “F reorganization,” a tax-free corporate reorganization under Internal Revenue Code (IRC) § 368(a)(1)(F). The IRC defines an F reorganization as a mere change of identity, form or place of organization of a corporation.1

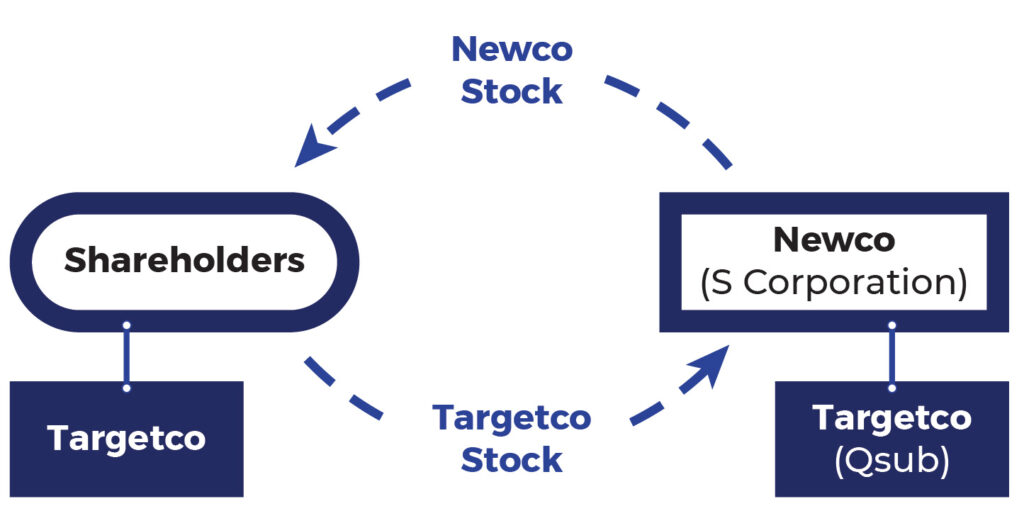

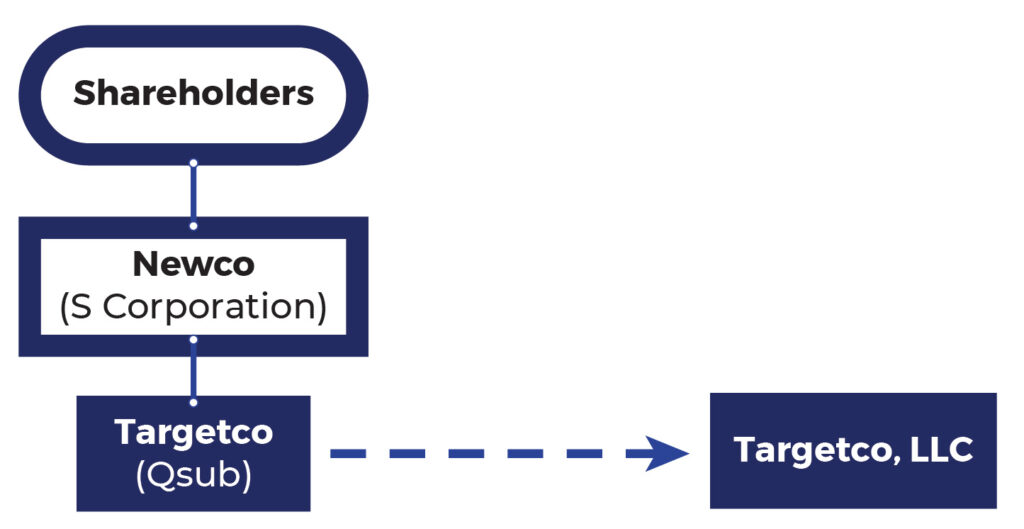

After undergoing an F reorganization, the target company may become a different type of entity, such as a limited liability company, and may be incorporated in another state. It will become a wholly owned subsidiary of a newly formed corporation (“Newco”). The steps to reach this result are as follows. First, the seller forms Newco as an S corporation. Second, the shareholders of the target company contribute all their shares to Newco in exchange for the stock of Newco. Newco elects to treat the target company, the shares of which it now owns, as a qualified subchapter S subsidiary (“Qsub”) so that it becomes a disregarded entity for federal income tax purposes. Third, the target company converts into a limited liability company under state law or merges into another subsidiary LLC formed in Delaware and remains a disregarded entity for federal income tax purposes.

The following diagrams illustrate steps 2 and 3:

Step Two

Step Three

As a result of the reorganization, the individual shareholders own all the equity of Newco in the same proportions that they owned the target company. Newco is the single member of the target company and now is the seller in the proposed business sale transaction. After the reorganization, the target company is now an LLC and becomes attractive to a wider array of buyers because the restrictions under Subchapter S of the IRC2 on who may own shares of the company no longer apply. Additionally, the target company is now a Delaware company.

Sometimes, the parties may want their transaction to include only some of the selling company’s assets. An F reorganization permits them to structure the transaction to sell less than all assets of the target business. To accomplish this, after the F reorganization is completed, the seller causes the target company to distribute up to Newco the assets that it wishes to retain. Then, only the assets that the buyer wishes to acquire will remain in the target company before the buyer purchases it. The F reorganization benefits both parties in this situation by enabling them to accommodate their business goals of transferring only some of the target company’s assets.

An F reorganization offers other benefits as well. After an F reorganization, the seller can treat the business transaction as a sale of equity interests, while the Buyer can treat it for tax purposes as an asset purchase transaction. For the seller, at least part of the sale proceeds may be subject to long term capital gains rates, which are lower than ordinary income tax rates. The buyer benefits from a step-up in the basis of the target’s assets equal to the purchase price. In addition, the buyer does not need to obtain third party consents associated with transferring assets (rather than equity interests). This can be valuable to the buyer of a health care provider, such as a clinical laboratory, by enabling the target company being acquired to retain any valuable health insurance and other third party payor contracts that it has in place.

A well-conceived F reorganization can offer buyers and sellers a valuable means to restructure target companies or buyer entities prior to business acquisitions to achieve various corporate and tax goals. The terms of such a restructuring can be specified in the parties’ purchase agreement and their implementation can be stated as a closing condition. Members of our firm’s corporate practice can help buyers or sellers of businesses use this corporate restructuring technique to reach agreement, maximize tax efficiencies and achieve other corporate goals in contemplated business acquisitions.