How Litigation Lawyers Protect Your Organization

In the dynamic and competitive business landscape, disputes are an unfortunate reality. Whether it’s a contract breach, a shareholder disagreement, or an environmental concern, litigation can disrupt operations, damage your reputation, and erode your bottom line. At Bleakley Platt & Schmidt, LLP, our experienced litigation lawyers understand the unique challenges faced by corporations and are dedicated to providing comprehensive solutions.

What is Litigation?

Litigation is the legal process of resolving disputes through the court system. It involves various stages, including filing lawsuits, a discovery phase for exchanging information, presentation of arguments, trial, and appeal. While most cases ultimately settle through alternative means like negotiation, mediation, or arbitration, understanding the litigation process is crucial for effective dispute resolution.

Dive deeper into the field of litigation here.

Bleakley By Your Side

BPS’s business litigation attorneys have a proven track record of success in complex matters. Our team represents businesses of all sizes, from Fortune 500 companies to local startups. We offer a comprehensive approach, including:

- Litigation Avoidance: We believe the best defense is a good offense. Our attorneys advise on contract formation, risk management, and negotiation strategies to minimize the chance of litigation.

- Pre-Litigation Strategy: When a dispute arises, our litigation lawyers can assess the situation, develop a winning strategy, and guide you through every step of the process.

- Cost-Effective Solutions: We understand litigation can be expensive, and work to achieve your goals while keeping costs in check.

- Extensive Experience: Our attorneys have deep expertise in various areas of business law, including contract disputes, shareholder and partnership disputes, mergers & acquisitions, intellectual property, and class actions.

Our litigation services, span more than a dozen practice areas. Here is a look at how BPS litigators apply their expertise to some of our largest practices:

Health Care Litigation: Navigating Complex Regulatory Waters

The healthcare industry is subject to a complex and ever-changing regulatory environment. Disputes involving hospitals, nursing homes, healthcare providers, and other healthcare entities require specialized knowledge and experience. BPS’s Health Care Litigation Practice Group provides comprehensive legal counsel to protect your interests.

Our attorneys represent clients in a wide range of matters, including:

- Compliance and Regulatory Investigations: We help healthcare providers navigate complex regulatory compliance issues and conduct internal investigations related to Medicare, Medicaid, fraud/abuse allegations, and false claims.

- False Claims Act: We have a strong track record of defending healthcare providers against allegations of fraud and abuse.

- Medicare and Medicaid Reimbursement: We assist clients in maximizing reimbursement and resolving disputes with government payers.

- Licensing and Certification Issues: We help healthcare providers obtain and maintain necessary licenses and certifications.

Corporate Litigation: Protecting Your Business Interests

Corporate litigation encompasses a broad range of disputes involving companies, shareholders, directors, and officers. Our Corporate Law Practice Group has extensive experience handling complex business disputes, including:

- Merger and Acquisition Litigation: We assist clients in resolving disputes related to mergers, acquisitions, and corporate control.

- Contract Disputes: We help businesses enforce their rights and protect their interests in contract disputes.

- Complex Commercial Litigation: We handle complex litigation matters involving multiple parties and high stakes.

Environmental Litigation: Mitigating Risks

Environmental compliance and litigation are critical concerns for businesses operating in today’s regulatory landscape. BPS’s Environmental Law Practice Group provides comprehensive legal counsel to help you manage environmental risks and protect your company’s reputation.

Our attorneys have extensive experience in:

- Superfund Litigation: We represent clients in complex Superfund matters, including site assessments, remediation, and cost recovery.

- Environmental Compliance: We assist clients in developing and implementing compliance programs to avoid costly litigation.

- Permitting and Regulatory Compliance: We help clients obtain necessary permits and comply with environmental regulations.

- Environmental Cleanup and Remediation: We provide strategic guidance on environmental cleanup and remediation projects.

- Natural Resource Damages: We defend clients against claims for natural resource damages.

Bleakley Platt & Schmidt: Your Trusted Litigators

At BPS, we are committed to providing exceptional legal representation and strategic guidance to our clients. Our litigation lawyers have the knowledge, experience, and resources to help you navigate complex legal challenges and achieve your business objectives. Contact our Litigation Practice Group today.

Read More

F Reorganizations Can Benefit Buyers and Sellers in Business Acquisitions

Certain corporate characteristics of a target company may be undesirable to potential buyers preventing them from acquiring the company. For example, the target company may be an S corporation, and the potential buyer would not qualify to be a shareholder of an S corporation under Internal Revenue Service (IRS) rules. Alternatively, the buyer may want the target company to be incorporated in a different state, such as Delaware, due to that state’s well-developed corporate law and chancery court system. In such situations and others, the seller can remove these obstacles prior to a sale by performing an “F reorganization,” a tax-free corporate reorganization under Internal Revenue Code (IRC) § 368(a)(1)(F). The IRC defines an F reorganization as a mere change of identity, form or place of organization of a corporation.1

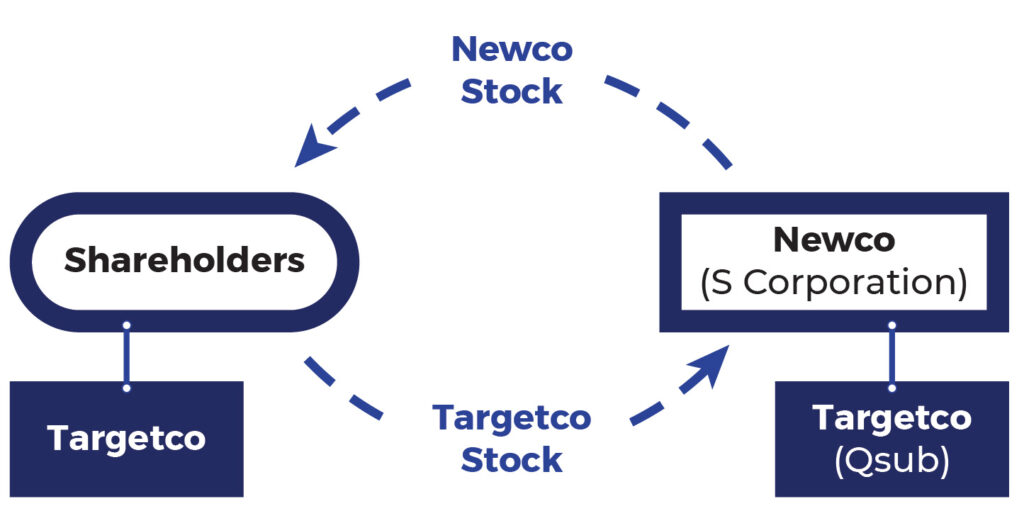

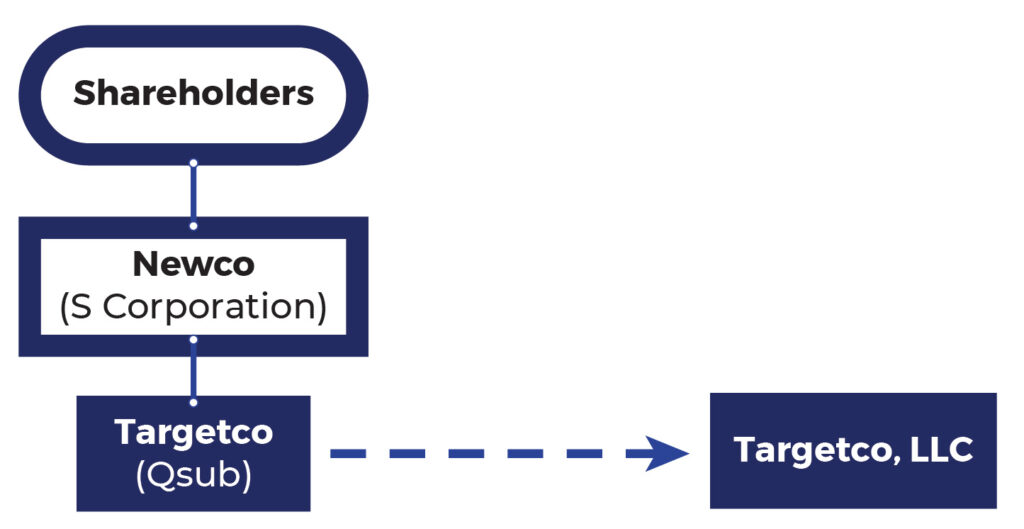

After undergoing an F reorganization, the target company may become a different type of entity, such as a limited liability company, and may be incorporated in another state. It will become a wholly owned subsidiary of a newly formed corporation (“Newco”). The steps to reach this result are as follows. First, the seller forms Newco as an S corporation. Second, the shareholders of the target company contribute all their shares to Newco in exchange for the stock of Newco. Newco elects to treat the target company, the shares of which it now owns, as a qualified subchapter S subsidiary (“Qsub”) so that it becomes a disregarded entity for federal income tax purposes. Third, the target company converts into a limited liability company under state law or merges into another subsidiary LLC formed in Delaware and remains a disregarded entity for federal income tax purposes.

The following diagrams illustrate steps 2 and 3:

Step Two

Step Three

As a result of the reorganization, the individual shareholders own all the equity of Newco in the same proportions that they owned the target company. Newco is the single member of the target company and now is the seller in the proposed business sale transaction. After the reorganization, the target company is now an LLC and becomes attractive to a wider array of buyers because the restrictions under Subchapter S of the IRC2 on who may own shares of the company no longer apply. Additionally, the target company is now a Delaware company.

Sometimes, the parties may want their transaction to include only some of the selling company’s assets. An F reorganization permits them to structure the transaction to sell less than all assets of the target business. To accomplish this, after the F reorganization is completed, the seller causes the target company to distribute up to Newco the assets that it wishes to retain. Then, only the assets that the buyer wishes to acquire will remain in the target company before the buyer purchases it. The F reorganization benefits both parties in this situation by enabling them to accommodate their business goals of transferring only some of the target company’s assets.

An F reorganization offers other benefits as well. After an F reorganization, the seller can treat the business transaction as a sale of equity interests, while the Buyer can treat it for tax purposes as an asset purchase transaction. For the seller, at least part of the sale proceeds may be subject to long term capital gains rates, which are lower than ordinary income tax rates. The buyer benefits from a step-up in the basis of the target’s assets equal to the purchase price. In addition, the buyer does not need to obtain third party consents associated with transferring assets (rather than equity interests). This can be valuable to the buyer of a health care provider, such as a clinical laboratory, by enabling the target company being acquired to retain any valuable health insurance and other third party payor contracts that it has in place.

A well-conceived F reorganization can offer buyers and sellers a valuable means to restructure target companies or buyer entities prior to business acquisitions to achieve various corporate and tax goals. The terms of such a restructuring can be specified in the parties’ purchase agreement and their implementation can be stated as a closing condition. Members of our firm’s corporate practice can help buyers or sellers of businesses use this corporate restructuring technique to reach agreement, maximize tax efficiencies and achieve other corporate goals in contemplated business acquisitions.

Read More

Implications of DOJ’s Whistleblower Pilot Program

The Department of Justice’s (DOJ) Criminal Division recently launched a Pilot Program on Voluntary Self-Disclosures for Individuals (the “DOJ Whistleblower Pilot Program“). This program encourages individuals with knowledge of federal corporate or financial misconduct to assist federal agencies without fear of prosecution. For U.S. financial institutions, navigating this new program and its implications requires careful consideration. According to the DOJ, the pilot program aims to fill in the “patchwork quilt” of existing whistleblower programs currently in place at other federal agencies, including the Securities and Exchange Commission (SEC), to ensure that all areas of criminal wrongdoing prosecuted by the DOJ are covered.

Program Summary

This federal whistleblower protection offers Non-Prosecution Agreements (NPAs) to individuals who meet specific criteria. DOJ may forgo criminal prosecution exchange for:

- Voluntarily disclosing original information about previously unknown corporate criminal conduct in violation of applicable U.S. law

- Cooperating with investigations

- Remedying any wrongdoing (i.e. returning profits from illicit activity and paying damages to victims)

Read a full synopsis of the program here.

Covered Criminal Conduct and Eligibility

The program focuses on specific areas of enforcement, including fraud, Foreign Corrupt Practices Act (FCPA) violations, and money laundering. Individuals who participated in the misconduct but can provide substantial assistance against higher-level culprits are eligible. The organizers of such illicit activities, however, are ineligible, as are CEOs and CFOs.

Background and Rationale

The DOJ recognizes the challenges of uncovering complex corporate crimes in violation of U.S. law. By offering new federal whistleblower protections, the program aims to:

- Increase Detection: Individuals with firsthand knowledge can provide crucial details that might otherwise go undetected.

- Enhance Investigations: Whistleblower cooperation strengthens cases against more culpable individuals.

- Promote Accountability: The program incentivizes companies to implement strong compliance programs that prevent and address misconduct.

Implications for Financial Institutions

Financial institutions subject to U.S. law face heightened scrutiny due to susceptibility to white-collar crimes. The DOJ Whistleblower Pilot Program presents both challenges and opportunities:

- Increased Risk of Disclosure: The program may embolden whistleblowers to come forward, potentially leading to more internal investigations.

- Importance of Compliance Programs: Robust compliance programs deter misconduct in the first place.

- Cooperation as a Defense Strategy: If an investigation arises, cooperating with the DOJ and demonstrating a commitment to compliance can be advantageous.

Considerations for Staying Compliant

Financial institutions subject to U.S. law should take proactive steps to address the DOJ Whistleblower Pilot Program:

- Review and Update Compliance Programs: Ensure programs effectively address the covered criminal conduct outlined in the program.

- Reinforce Internal Reporting Mechanisms: Provide clear and accessible channels for employees to report suspected wrongdoing internally.

- Anti-Retaliation Policies: Uphold strong anti-retaliation policies to protect employees who report misconduct in good faith.

This latest federal whistleblower protection signifies a shift in the government’s approach to investigating and prosecuting corporate crime. Financial institutions can reduce risk by understanding the program’s impact and promoting a culture of compliance. For more information, contact Jennifer A. Lofaro of our Commercial Finance Practice Group at (914) 287-6136 or jlofaro@bpslaw.com.

Read More

New York LLC Transparency Act vs. Federal Corporate Transparency Act: A Guide for New York LLCs

The recently enacted New York LLC Transparency Act (NY LLCTA) was amended by Gov. Hochul at last month. It is based on the federal Corporate Transparency Act (CTA), and as such, bears significant similarities. However, the two acts are nonetheless distinct and have different scopes and timeframes. Here is a look at NY LLCTA, how it compares with CTA, and how businesses can remain compliant with both.

Understanding the New York LLC Transparency Act

The NY LLCTA, effective Jan 1, 2026, mandates the reporting of beneficial ownership information for limited liability companies (LLCs) formed or qualified to do business in New York State. This means LLCs must disclose details about individuals who own and control 25% or more of the company’s voting interests or profits.

Key Requirements of the New York LLC Transparency Act

- Reporting Entities: All LLCs formed in New York or registered to do business within the state are required to file a beneficial ownership report (BOR) with the New York Department of State (DOS).

- Beneficial Ownership Information: The BOR must include the name, date of birth, residential address, and a unique identifying number (issued by the IRS) for each beneficial owner.

- Exemptions: Certain types of LLCs are exempt from the NY LLCTA’s reporting requirements. These include publicly traded companies, certain investment funds, inactive businesses, and entities exempt from CTA.

How Does the New York LLC Transparency Act Differ from the Corporate Transparency Act?

While the NY LLCTA shares similar goals with the federal CTA, there are some key distinctions:

- Scope: The NY LLCTA applies solely to New York LLCs, whereas the CTA covers a broader range of business entities, including corporations.

- Exemption Filings: Unlike the CTA, the NY LLCTA requires exempt LLCs to file a certification with the DOS claiming their exemption.

- Public Access: A significant difference lies in public access to the reported information. The NY LLCTA initially proposed a public database, but this has been put on hold. Conversely, the CTA mandates a secure, government-only database for BOR information.

- Filing Deadlines: As per the NY LLCTA, businesses formed or qualified to do business in New York State on or after Jan. 1, 2026 will have 30 days to comply, while those formed or qualified prior to that date will have until Jan. 1, 2027. Under the CTA, reporting companies formed prior to Jan. 1, 2024 have until Jan. 1, 2025 to comply, while companies formed Jan. 1, 2024 through Dec. 31, 2024 have 90 days to comply. Those formed on or after Jan. 1, 2025 have 30 days.

- Correction Timeframes: The NY LLCTA allows for corrected reports to be filed within 90 days of submission, while the CTA has a tighter 30-day window.

- Penalties: The NY LLCTA imposes a $250 civil penalty for non-compliant LLCs after two years of delinquency. Additional fines of $500 per day may be accrued for each day past due. The CTA carries potentially harsher civil and criminal penalties for non-compliance.

Complying with Both Acts: How BPS Can Help

Since both the New York LLC Transparency Act and the Corporate Transparency Act may apply to your LLC, it’s crucial to understand the requirements of each act and ensure compliance with both.

The veteran attorneys of our Corporate Law Practice Group can assist your LLC with navigating the nuances of these similar acts. Contact Robert Braumuller at (914) 287-6185 or rbraumuller@bpslaw.com to stay compliant.

Read More